Health Savings Accounts (HSAs) are often viewed as a short-term healthcare spending tool. However, for high-income earners and strategic savers, HSAs can be one of the most tax-efficient retirement accounts available. With the right planning, an HSA can function as a triple-tax-advantaged account, complementing IRAs and 401(k)s in your long-term financial strategy.

What is an HSA?

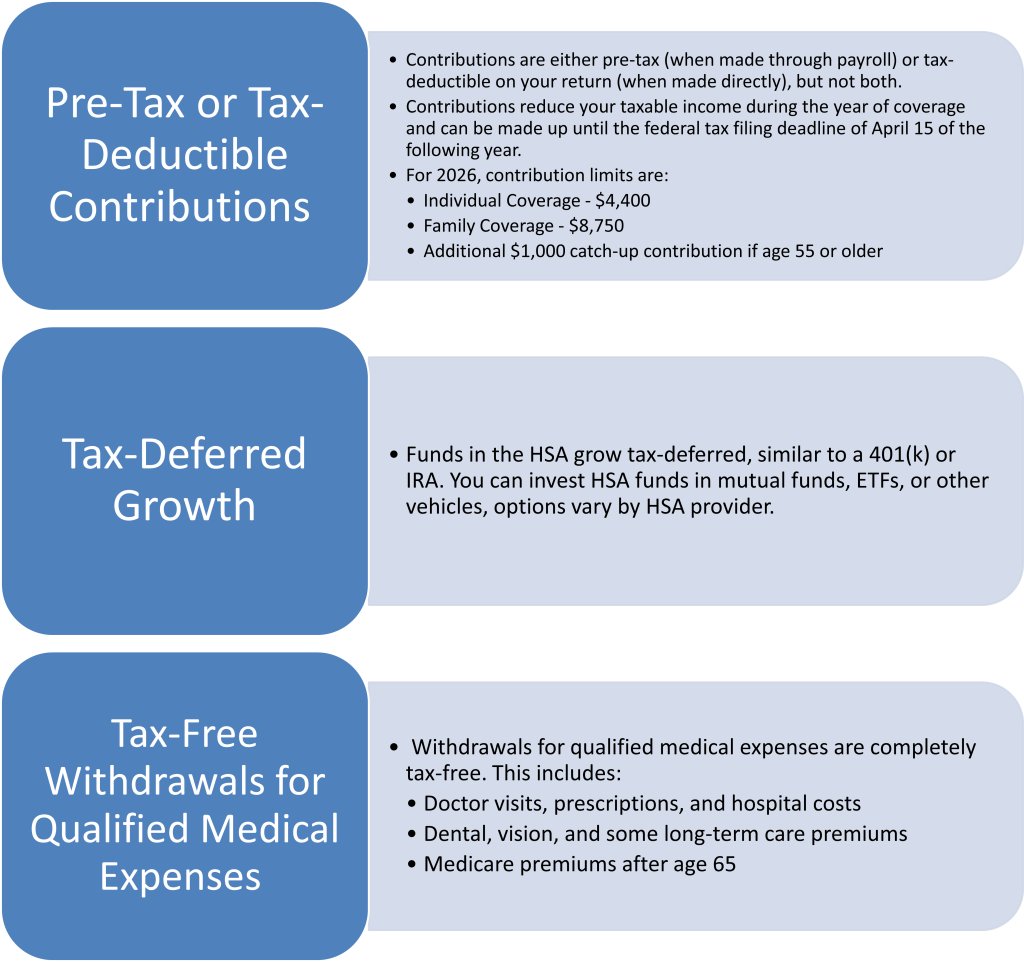

An HSA is a tax-advantaged savings account paired with a High-Deductible Health Plan (HDHP). HSA contributions reduce taxable income (generally made through payroll deductions or direct deposits into the account), grow tax-deferred, and can be withdrawn tax-free for qualified medical expenses. Payroll contributions made through a cafeteria (Section 125) plan carry an added advantage, as they also bypass Social Security and Medicare taxes. It’s also important to note that any employer contributions to your HSA count toward the annual IRS contribution limit, so you’ll need to factor those in when determining how much you can personally contribute each year.

However, there are a few key requirements to keep in mind when making contributions:

- You must be enrolled in a qualified HDHP (defined in 2026 as a plan with a minimum deductible of $1,700 for individual coverage or $3,400 for family coverage, and out-of-pocket maximums not exceeding $8,500 for individuals or $17,000 for a family).

- You cannot be claimed as a dependent on someone else’s tax return.

- No other health coverage while contributing (except for certain exceptions, e.g., dental, vision, long-term care)

- Enrolling in Medicare ends your ability to contribute to an HSA, even if you’re still working and are covered by an employer-sponsored HDHP.

Unlike most savings and retirement accounts, HSAs offer three separate tax benefits that work together to maximize your long-term wealth.

While HSAs are designed around healthcare, their benefits extend well into retirement, making them one of the most versatile accounts in a long-term financial plan. After age 65, the rules around HSA withdrawals become significantly more flexible:

- Withdrawals for non-qualified medical expenses are taxed as ordinary income, similar to a traditional IRA. This means the withdrawal is added to your taxable income for the year and taxed at your marginal federal income tax rate, with no additional penalty.

- Withdrawals for medical expenses remain tax-free, including Medicare Part B, Part D, and Medicare Advantage premiums (but not Medicare Supplemental policies) along with some long-term care premiums.

- Long-term care premiums can be withdrawn tax-free at any age up to the deductible cap.

| Age | Maximum Deductible Premium (LTC) |

|---|---|

| 40 or younger | $500 |

| 41–50 | $930 |

| 51–60 | $1,860 |

| 61–70 | $4,960 |

| 71 or older | $6,200 |

- You can invest contributions for long-term growth, treating the HSA like a secondary retirement account.

This flexibility is why many financial advisors refer to the HSA as a “stealth IRA.” Unlike a traditional IRA, the HSA layers on the additional benefit of tax-free withdrawals for medical costs which is a meaningful advantage given that healthcare is typically one of the largest expenses retirees face.

Contribution Strategies

- Max out contributions early – Even if you don’t need the funds for current medical expenses, contribute to maximize tax-free growth.

- Invest the HSA funds – Many HSAs allow you to invest once your balance reaches a minimum threshold. Long-term investing can turn small contributions into a significant nest egg.

- Pay medical costs out-of-pocket, pay yourself back later – If possible, pay medical expenses out-of-pocket and let your HSA balance compound over time. You can reimburse yourself tax-free at any point in the future, even years later, as long as the expense was incurred after your HSA was originally opened.

Common Mistakes to Avoid

- Treating the HSA like a checking account instead of a long-term investment vehicle.

- Not investing the HSA funds once eligible.

- Failing to keep receipts for medical expenses if planning to reimburse later.

- Using the account for non-qualified expenses before age 65, which triggers taxes and a 20% penalty on the entire non-qualified withdrawal amount, not just the growth.

- Ignoring the last-month rule’s testing period requirement, additional contributions become taxable with a 10% penalty if HSA eligibility is not maintained through December 31st of the following year.

- This applies only to those who contribute the full annual amount during a year in which they were not HSA-eligible for the entire year (i.e., an individual who enrolls in an HDHP on December 1, 2025, and contributes the full annual amount for 2025 must remain HSA-eligible through December 31, 2026).

- Failing to coordinate contributions between spouses who are both enrolled in a HDHP, who share one family contribution limit.

HSA vs. Other Retirement Accounts

| Feature | HSA | Traditional 401(k)/IRA | Roth IRA | Roth 401(k) |

|---|---|---|---|---|

| Contributions | Pre-tax | Pre-tax | After-tax | After-tax |

| Growth | Tax-deferred | Tax-deferred | Tax-free | Tax-free |

| Withdrawals | Tax-free for medical | Taxable | Tax-free | Tax-free |

| Flexibility | Triple tax advantage, can reimburse past expenses | Limited to retirement | Limited to retirement | Limited to retirement |

| Penalty | 20% if used for non-qualified med exp prior to age 65 | 10% early withdrawal | No early withdrawal of contributions | 10% early withdrawal |

HSA vs. FSA: What’s the Difference?

Flexible Spending Accounts (FSAs) are frequently confused with HSAs, but they operate quite differently. An FSA does not require enrollment in an HDHP, making it accessible to a broader range of health plan participants. However, FSAs come with a significant limitation, they are “use it or lose it” accounts, meaning funds that are not spent by the end of the plan year are generally forfeited, with only a limited rollover allowed at the employer’s discretion. HSAs, by contrast, carry over indefinitely and can grow and compound over time. It is also important to note that you cannot contribute to both an HSA and a general-purpose FSA simultaneously (though limited-purpose FSAs for dental and vision are allowed), enrolling in one typically disqualifies the other.

HSAs provide unique advantages, especially for those with high-deductible health plans and a focus on tax-efficient wealth building.

An HSA is more than a healthcare account; it’s a powerful, flexible, and tax-efficient tool for retirement planning. By contributing, investing, and strategically timing withdrawals, an HSA can supplement your 401(k), IRA, and Roth strategies, offering a triple-tax benefit rarely available in other accounts.

High-income earners and retirees should treat their HSA as a long-term investment vehicle, not just a short-term spending account. With careful planning, an HSA can help fund medical expenses in retirement while building a tax-advantaged nest egg.

While HSAs offer compelling long-term tax advantages, they are not the right fit for everyone. For individuals with high ongoing medical costs, a low-deductible plan may result in lower total out-of-pocket spending throughout the year, potentially outweighing the long-term tax benefits of an HSA-paired HDHP. The math shifts when current healthcare expenses are significant enough that the higher deductible of an HDHP creates a meaningful financial burden. Before defaulting to an HSA strategy, it is worth modeling your expected annual medical costs against the total cost structure of each plan to determine which option is most advantageous for your specific situation.

Ready to put your HSA to work as part of a broader retirement strategy? Contact us to connect with a Goodman Financial advisor.

Goodman Financial Corporation is a fee-only Registered Investment Adviser (RIA). Registration as an adviser does not connote a specific level of skill or training. More detail, including form ADV Part 2A filed with the SEC, can be found at https://adviserinfo.sec.gov/. Neither the information, nor any opinion expressed, is to be construed as personalized investment, tax, or legal advice. The accuracy and completeness of information presented from third-party sources cannot be guaranteed. This firm is not a CPA firm.