APRIL 2026 MARKET COMMENTARY

EQUITY & FIXED INCOME MARKETS

The markets continued to shrug off the fluctuations of the Iran crisis and rallied around strong corporate earnings and traction in the Artificial Intelligence (AI) sector. Led by the Information Technology (IT) sector, the S&P 500 Index rose 5.3%, while the Dow was up 2.9% and the Nasdaq Composite 8.4%. Mid- and small-cap stocks also rose, with the S&P 400 Mid-Cap Index up 2.5% and the S&P 600 Small-Cap Index up 1%. International markets were positive as well, with developed markets ex-U.S. up 2.6% and emerging markets up 9.5%. Against this backdrop, GFC’s Equity Composite rose 1.93% net of fees for April, underperforming the S&P 500 in relative terms. GFC’s Fixed Income Composite returned 0.3% net of fees, outperforming its benchmark return of 0.1%.

On a year-to-date basis, GFC’s Equity Composite is up 10.9% net of fees, slightly under the S&P 500 which is up 11.3%, above the Dow at 6.9%, and under the Nasdaq at 16.3%. GFC’s Fixed Income Composite is up 0.6% year-to-date net of fees versus a 0.3% return for its benchmark.

MAY FLOWERS

While the equity markets have rallied at a torrid pace, May’s performance was isolated to AI-related stocks in the IT sector. The IT sector, up +16% for the month, was the only sector to outperform the S&P 500 return in May. One of the narratives around the recent market rally has been the strength of U.S. corporate earnings. While that is generally correct, we also noticed a divergence in earnings growth between IT and other sectors. For example, the S&P 500 posted a blended earnings growth of nearly 29% this earnings season, the best since 4Q 2021. But in looking under the hood, the IT-heavy Magnificent Seven companies showed +63% earnings growth vs. the remaining 493 companies showing +17% earnings growth. The IT sector weight inside the S&P 500 is now over 37%, which is an all-time high and even higher than the Dot-Com Bubble peak of 35%.

Narrow stock market rallies tend to lead to increased gambling by short-term oriented investors. Margin debt has increased over 50% in the last year and is now over 5% of U.S. GDP, which is a new record. Trading volumes in leveraged ETFs, ones that will give 2x or 3x the return of an underlying stock, have increased significantly over the last few months. Adding fuel to the fire may be the upcoming IPOs of SpaceX, OpenAI, and Anthropic as we would expect a FOMO (Fear Of Missing Out) frenzy to grip the markets over the second half of the year. While these companies are already large in scope (SpaceX could be one of the ten largest stocks in the U.S. at the IPO), we would exercise caution due to some red flags we are seeing in corporate governance.

- SpaceX will have a dual share class structure, where Elon Musk would personally hold Class B “super-voting” shares, which would give him ten times the voting power of Class A shareholders (everyone else). Caution is warranted when shareholders do not have the ability to influence necessary changes, and there is significant “key person” risk at SpaceX.

- OpenAI was originally structured as a non-profit foundation. Ahead of the IPO, it recently restructured to a for-profit enterprise with the original non-profit foundation still retaining a 26% equity stake but keeping significant structural control. For example, the legacy non-profit foundation appoints all members of the Board of Directors in the new for-profit entity and retains the unilateral right to replace them at any time. There is also significant overlap with CEO Sam Altman and others serving on the boards of both entities.

- Anthropic has created a “Long-Term Benefit Trust” that is meant to balance the fiduciary duty of maximizing profits for shareholders with public safety around Artificial Intelligence. While the intention is sound, the structure is vulnerable to be dismantled by a “supermajority” of shareholders. Anthropic has not released actual numbers around this “supermajority” nor the full verbiage around the Trust Agreement, which has led corporate governance experts to question its broader mandate.

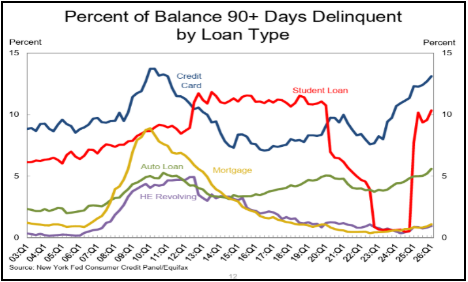

While the equity markets continue this historic rally, the average consumer remains stretched. The latest inflation print showed increases in food and gas prices as a result of the Iran crisis. If the crisis continues past the summer, the current oil stockpiles used to keep energy prices somewhat stable may not last. The attached chart already shows upticks in delinquent loans for consumer credit cards, autos, and mortgages. This increased consumer stress may show up in the upcoming U.S. mid-term elections, with the risk that a change in leadership in the House and Senate would lead to many of the corporate tax benefits found in the One Big Beautiful Bill being paused or outright repealed.

For this equity rally to continue for the rest of the year, we believe we would need to see (1) a broader market rally with more participants than just the IT sector (2) a swift resolution to the Iran crisis and (3) a tempering of the excessive valuations recently seen in the IT sector and predicted for the upcoming IPOs mentioned above. To quote Oscar Wilde on the excesses of a prior era, “Nowadays people know the price of everything and the value of nothing.”

Robin Kollannur, CFA

Chief Investment Officer