Cost of Corporate and Municipal Bonds")

The True¹ (and Usually Hidden) Cost of Corporate and Municipal Bonds

The corporate and municipal bond markets have long been the land of milk and honey for many brokerage firms. These markets are less transparent and less regulated than the equity market, which means more profits for brokers. Also, bonds are often overlooked in comparison to stocks. They are complicated, have a fixed return, and don’t get as much scrutiny as their pricing is more stable than stocks. They play a quintessential role in reducing risk in a portfolio, but let’s face it, most non-dorks think bonds are boring. I think they’re fascinating. In contrast, stocks are exciting with high potential returns over the long run, daily volatility, and are gruelingly covered by the minute on CNBC. Because bonds are not given nearly the attention, brokers have been able to charge high fees on the purchase and sale of such securities. Even worse, the markup on bonds is embedded in the price and is therefore undisclosed and unseen by the investor. Add that to the fact that most investors wouldn’t know if they’re getting a good deal on a bond because who actually checks the prices? (We do.) Bond traders are required to give a “fair and reasonable” price on a bond, but “fair and reasonable” is up for interpretation and highly subjective. Consider the following hypothetical example. John calls Broker A to buy a $10,000 bond investment (10 bonds) with a “good” fixed return.

Broker A finds one and reports a price of $10,655 with a yield of 3.0% per year until 2020. John is happy with the statistic, gives his consent, and the deal is done.

John sleeps well knowing he will receive a fixed return, barring a default. But, John has no idea if he’s getting a good deal because 1) John doesn’t know the true value of the bond determined by recent market activity and the relative risk of the bond; 2) John doesn’t see the markup on the bond because it’s embedded in the price; and 3) John doesn’t know if this bond is the best bond for him based on his risk tolerance. Let’s take a look at the other side of the equation. Broker A is constantly changing its inventory of bonds to provide for clients (normal course of business for broker-dealers). On Tuesday morning, Broker A purchases a $10,000 par value bond for $10,500 for its internal inventory. This is called principal trading (still normal). The brokerage firm is now able to offer it to its clients and take a profit for providing the service (reasonable). John, our retail investor, calls five minutes later and the bond is quoted at $10,655. Did the bond instantaneously appreciate by $155 in those five minutes? Highly unlikely. If we take the same example for 100 bonds ($100,000 par value), that’s $1,550 instantly pocketed by the brokerage firm. Further, there is a potential conflict of interest because Broker A benefits from the trade regardless of whether it was the most suitable bond for John’s portfolio.

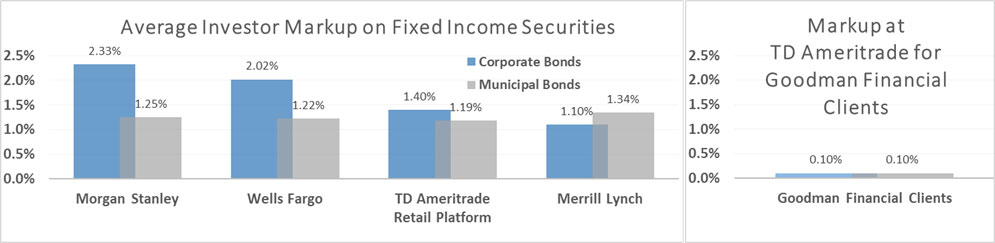

It’s wrong to suggest that brokerage firms should not make money on trading or that brokers have conflicted interests, but investors need an advocate for more reasonable bond prices and trades that don’t carry any conflict of interest. At Goodman Financial, through our primary custodian, TD Ameritrade, the cost to clients is $1 per $1,000 bond, or one-tenth of one percent (almost 15x less than the average markup at some other firms). To put this into perspective, a 0.10% markup (also known as ten basis points) has an impact of approximately 0.02% per year on the yield of a five-year bond. See the chart below for the results of a study on bond markups combined with the rates our clients are charged. A bond purchase with a value of $2,000 costs our clients $2, or two cheeseburgers from the dollar menu. Further, to trade a $100,000 bond costs our clients $100, whereas such markup at an industry-wide average would be $1,480.² And, we do not benefit from the purchase or sale of said bonds or any other client transactions, and are only compensated by our investment-advisory fees.

So, here are a few questions to ask your advisor or broker when you are buying bonds or when bonds are purchased on your behalf.

- What’s the embedded markup on these bonds? (There is almost always a markup so don’t take “no markup” for an answer.)

- Are there any additional costs of this trade?

- When did this bond most recently trade? And, for what price?

- Is the risk of this bond consistent with my risk profile?

Source: Fidelity Investments; fidelity.com/go/bond

¹ I was hoping you’d notice my footnote. Footnotes are used excessively in the financial services industry, partly due to important and necessary regulations; however, they can also be used by brokers to state extra costs beyond the “quoted” price of a security. You can now return to the article so I can further explain.

² A recent study by Fidelity found that among four major markup-based firms the average markup on thousands of corporate and municipal bonds studied was 1.48% in late 2015. The markup ranged from 1.10% to 2.33%. See the graph above for a graphical representation.

{kind=link}